Like most homeowners, you could probably look around your property and see some things you’d like to change. Whether it’s fixing up the place, adding new features or increasing your living space, there’s no shortage of ideas. The trick is how to pay for them.

Home equity is naturally the go-to resource for home improvement loans, but it’s not an option that’s always available. If it’s not, a viable option to consider might be using a personal loan for home improvement financing.

Find personal loans for home improvement

Using a personal loan for home improvement

Personal loans are similar in structure to a mortgage or an auto loan in that they usually come with fixed interest rates and payments. They differ in that personal loans do not require collateral. For such unsecured loans, qualifying depends heavily on your credit history and financial situation.

Another characteristic of unsecured loans is that they demand higher interest rates than secured loans. That’s because the lender does not have any collateral to fall back on should the borrower default. According to the Federal Reserve, in 2018 the average personal loan rate was 10.70%. At that time, 30-year mortgage rates averaged around 4.78% and rates charged on credit card balances averaged 16.86%.

This shows that while personal loans may be more expensive than mortgages, on average they are considerably cheaper than another unsecured alternative, which is borrowing against your credit card. And mortgages can carry very high setup costs — an important factor in the decision to use a personal loan for home improvements.

Related: Personal Loan Interest Rates (How to Pay Less)

When should you use a personal loan for home improvements?

If the following circumstances describe your situation, a personal loan might be the right option for financing your home improvement:

You have little or no home equity

In many (probably most) cases, a home equity loan is cheaper than a personal loan for a home improvement project. But its availability would depend on how much equity you have in your home. Naturally, if there is little or no equity to borrow against, a home equity loan is not an option.

If you do not have sufficient equity to get a home equity loan, then a personal loan becomes a viable option because it should be significantly cheaper than borrowing against your credit card to finance home improvements.

The amount needed is relatively small

Some home equity loans, especially fixed-rate products, come with most of the same fees a mortgage has — title and escrow charges, lender fees, home appraisal fees and other costs. Even Home Equity Lines or Credit (HELOCs) can require a home appraisal that costs hundreds of dollars, and / or have set-up costs of about $500.

If you only need a few thousand dollars, a personal loan may be cheaper despite its higher interest rate.

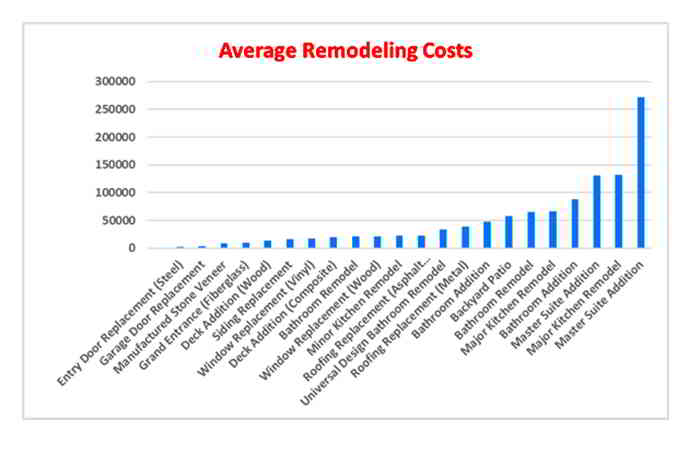

The table below shows average costs for renovations, courtesy of Remodeling Magazine. Less-expensive projects may be better-suited to a personal loan than a second mortgage.

You have limited liquid assets

Because there is a cost to borrowing money, it’s good to consider using savings for your project. With personal loan rates averaging more than ten percent and savings account rates averaging less than one percent, it is more cost-effective to take money out of savings than to borrow.

With that said, you should always keep enough savings on hand to prepare for financial emergencies. And hitting your retirement account is a bad choice if you can’t avoid the tax consequences.

You have good credit

A personal loan is a viable option if you have good credit, which is generally considered to be a credit score of 670 or better. You might get a personal loan with a lower credit score, but it is likely to cost you in the form of a significantly higher interest rate. For this reason, be sure to review your credit report before you apply for a loan, to see if there are any problems you can clear up to improve your score.

Related: What Credit Score Is Needed for a Personal Loan?

The payment plan fits your budget

With any loan, the practicality of it is not just a matter of whether you can qualify for the loan, but also how readily the payments will fit into your budget. Before you commit, review a payment schedule and make sure you can afford it given your other financial commitments.

Also, consider how these payments might delay other plans, such as saving for retirement or to send your kids to college.

Home improvements can represent a sensible investment. They can make a home more enjoyable, more cost-effective or safer. They can even add to the value of the property. One component of making this investment workable is choosing the best way of paying for it, and under the right circumstances a personal loan could be the best option for you.